NHL News

Matt Perri analyzes Salary vs Cap Hit in Cap Relief Trades

Matt Perri, former Director of Analytics for the Arizona Coyotes, created the models for the PuckPedia Perri Pick Value Calculator and PuckPedia Perri Cap Relief Calculator. Check them out!

![]()

![]()

Matt Perri analyzes the impact on the Cap relief model of salary versus cap hit, and on draft picks in future years. Be sure to check out his related articles:

Matt Perri shares his Coyotes experience creating the Draft Pick Value Table

Matt Perri explains his Cap Relief Value model

Matt Perri reviews trade deadline

Market Value

Let’s talk about cap hit and salary.

If this article is of any interest to you, then I’ll assume you know that NHL contracts involve a cap hit and a salary. Player cap hits apply to a team’s cap situation, while salaries apply to a team’s payroll. I won’t get into the reason why we have separate variables for cap hit and salary, but we do, and the main difference between them is that cap hits never vary by season (per contract), while salaries are often structured to feature higher or lower amounts per season (so long as the average per year works out to equal the cap hit). Salary per season can also be split into a signing bonus (paid out on one day, usually July 1st), and base salary. Let’s not even get into performance bonuses…

The end result of all this is that at any point in time, a player’s cap hit owed can vary from their salary owed. This was a problem I could not solve for our cap relief model, so I designed it as a “cap-only” model that ignores cap/salary asymmetry issues.

Our model was extremely accurate at predicting this year’s double retention pick compensations (within 8.5 picks on average, plus or minus, if we project pick order based on PTS% rank as of each trade), but each of the four examples from this year’s deadline involved players whose cap hit owed was identical to their salary owed. Our model went untested as far as salary is concerned.

Cap vs Cash

Allow me briefly recount my troubles modeling salary relief. This is mostly technical and the story ends in failure.

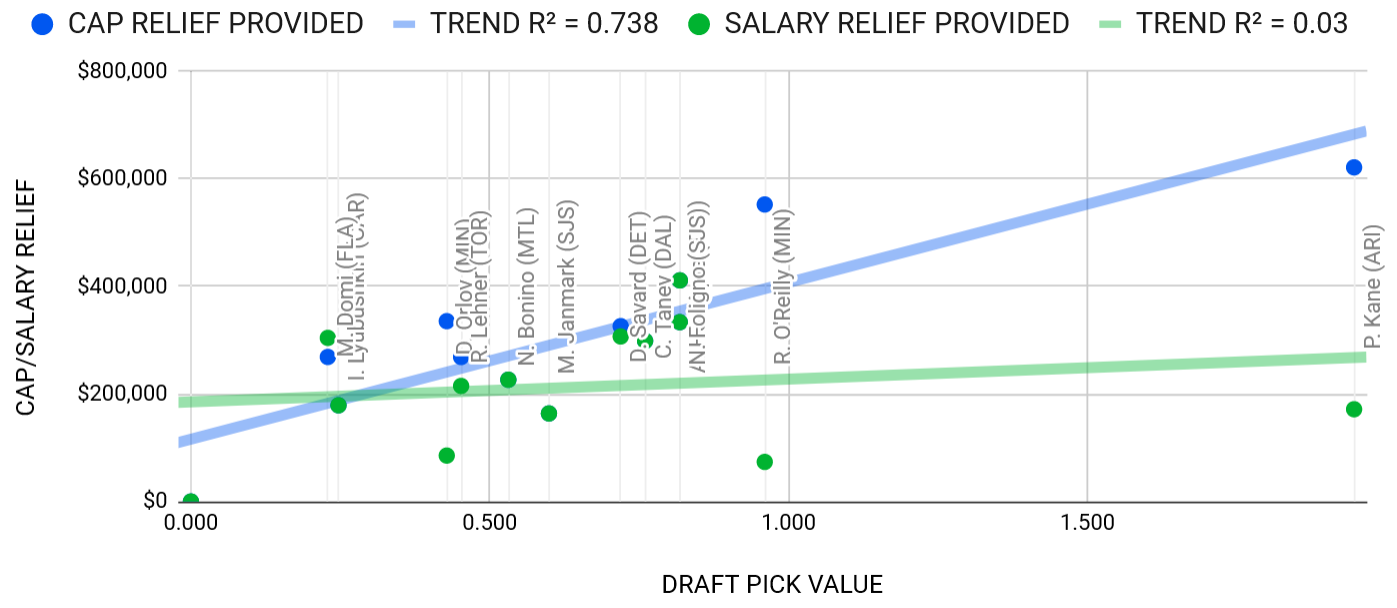

I started in the same place as the cap relief model — three team retention trades. These trades show a trend when modeling cap relief, but not so for salary relief:

We could remove two or three outliers to find a signal, but the problem is, those outliers are the deals that are most identifiable as “salary deals”. Their extremely low salary / cap owed ratio is what makes them so enticing to teams that care strongly about cash output. Removing them kind of defeats the purpose.

Adding in the cap dump trade dataset greatly boosted the strength of the salary trend, but the model it produced was nonsensical. Compared to the cap relief model, a pure salary relief model predicted a much higher draft capital return for amounts above $4.5M, but a much lower draft capital return for amounts below $4.5M. Most concerning, it performed worst for relief values below $2M.

I tried a multiple regression model, which can make a prediction based on cap relief and salary relief at the same time, but it didn’t do nearly as well as the cap relief only model. It also implied salary relief is statistically insignificant in predicting pick compensation (at least for this dataset).

I think a big part of the problem is that outliers in the data lead to high variance in draft capital return per salary relief. This variance is much greater than for cap hits, and datasets with large variance generally require larger sample sizes. Therefore, we would need more examples of salary relief than we have of cap relief to produce a model with similar predictive power.

That is, of course, assuming there is a signal to find. As I said in my last article, salary will matter in some trades but almost not at all in others, so it seems perfectly reasonable to me that unless we can isolate the trades in which salary mattered, we won’t be able to find a good signal.

Wild Speculation

Hopefully more data points from future trades will allow me to build a salary relief model. Until then, let’s speculate wildly.

If I had to hazard a guess, I would say that salary relief is probably worth more than cap relief. Why? Well, it all comes down to the data we’re looking at.

To build the cap relief model, I analyzed seventeen trades involving double retention or cap dumps. In this dataset, the salary owed was about 70% of the cap hit owed. This means that, compared to cap relief, lower amounts of salary relief are being traded for the same amount of draft capital. Thus, salary relief, measured on its own, seems to be worth more than cap relief.

It’s not surprising that the amount of salary owed in my dataset is less than the amount of cap owed. For one, double retention trades tend to involve contracts in their final season(s), which tend to have low salary/cap owed ratios due to the prevalence of front-loaded contracts. On top of that, remember that potential signing bonuses are paid out on one day (almost always July 1st), leaving just the base salary for the rest of the season.

To put it simply, the relative difference between salary owed and cap hit owed in the sample will hugely impact how much eating salary is worth relative to eating cap. If our sample contains a high proportion of low salary/cap owed contracts, then it would suggest that retaining salary is worth much more than retaining cap. If the sample contains a roughly balanced salary/cap owed ratio, then it would suggest retaining salary is roughly equal to retaining cap.

Theoretically, as our sample approaches all active contracts, we should see less bias towards front/back-loaded contacts, and thus our salary/cap owed ratio will move towards 1.0 (but never actually get there because of signing bonuses).

Now, this is very shaky ground here. I’m musing on a topic that doesn’t have enough data to furnish an opinion. But while we’re at it, what else can we speculate on?

Today vs Tomorrow

Moving on to another topic raised by some on Twitter — are draft picks in future years worth less than draft picks from this draft?

The right way to look at this would be to go back to our draft pick value model’s data set and build a new model that also teases out the value of future picks based on how far away they are from the trade. That’s a new model build that I’ll have to leave for the future.

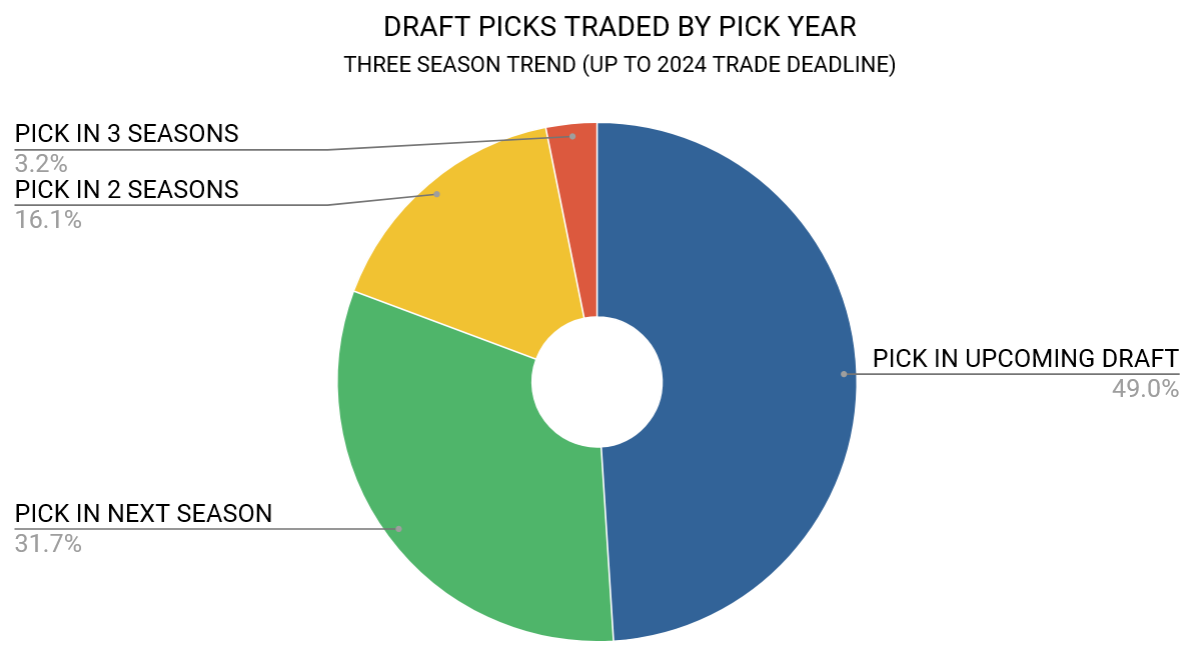

Until then, let’s look at it this way: NBA teams are trading picks six seasons into the future. At what rate do NHL teams deal picks from future years?:

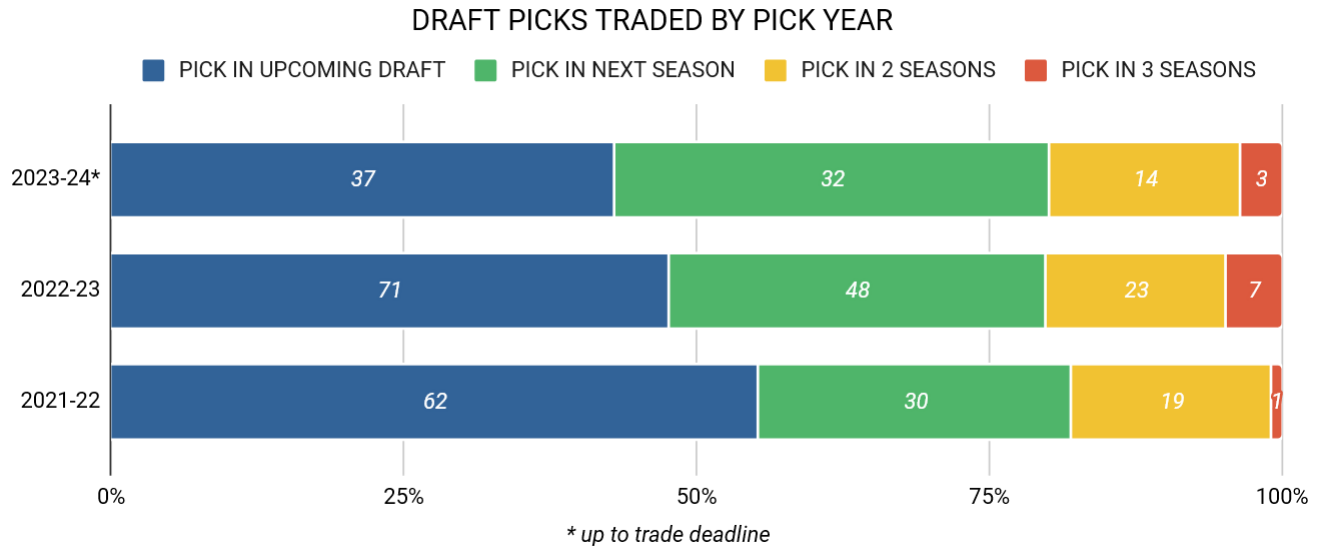

Over the last three seasons (up to this year’s trade deadline), roughly half of all picks exchanged were picks from that seasons’ draft, with picks less and less likely to be dealt the further they are from the present year.

I’m not surprised by this. NHL teams are conservative. My own view is that teams should be more willing to acquire future picks, and interestingly, it seems like they may be beginning to think the same:

The biggest trend here is that, season over season, teams are trading a higher proportion of picks from the next season’s draft than they used to, and a lower proportion from the upcoming draft.

Tomorrow Is a Long Time

I think there are a few major reasons why future picks are valued less.

Uncertainty of pick order is the best argument for lower value in future years. Especially in the first round, there is risk in the uncertainty in where a future pick will lie. This is why teams increasingly resort to complex conditions and protections to boost certainty when acquiring future picks. This is bad for fans — deals become even harder to understand — but it may also be bad for teams in the long run. More conditions means more future picks are tied up because those conditions have not been able to be met yet, and thus those picks are unable to be dealt, limiting a team’s options. This might begin to become an issue.

As for other reasons, well, ideally, the adage “a bird in the hand is better than two in the bush” should not apply to draft pick ownership. Aside from the odd punitive measure, pick ownership is secured by the NHL. They are the bank that teams hold their currency in, and they are Fort Knox.

In reality though, if you are a team that believes your window to win is now or at least very soon, you will obviously value future picks less. A late-round draft pick three years from now used on a player that will take at least three years to develop is not what you need now. Of course, these teams are also incentivized to trade away the current year’s picks, but those picks should theoretically hold slightly more value to them than future year picks because at least a player picked today can start their development now.

There are, of course, also teams that are planning to win later rather than now. These teams should want to acquire future draft capital because they need it, but also because their picks will likely be good (earlier in the draft order).

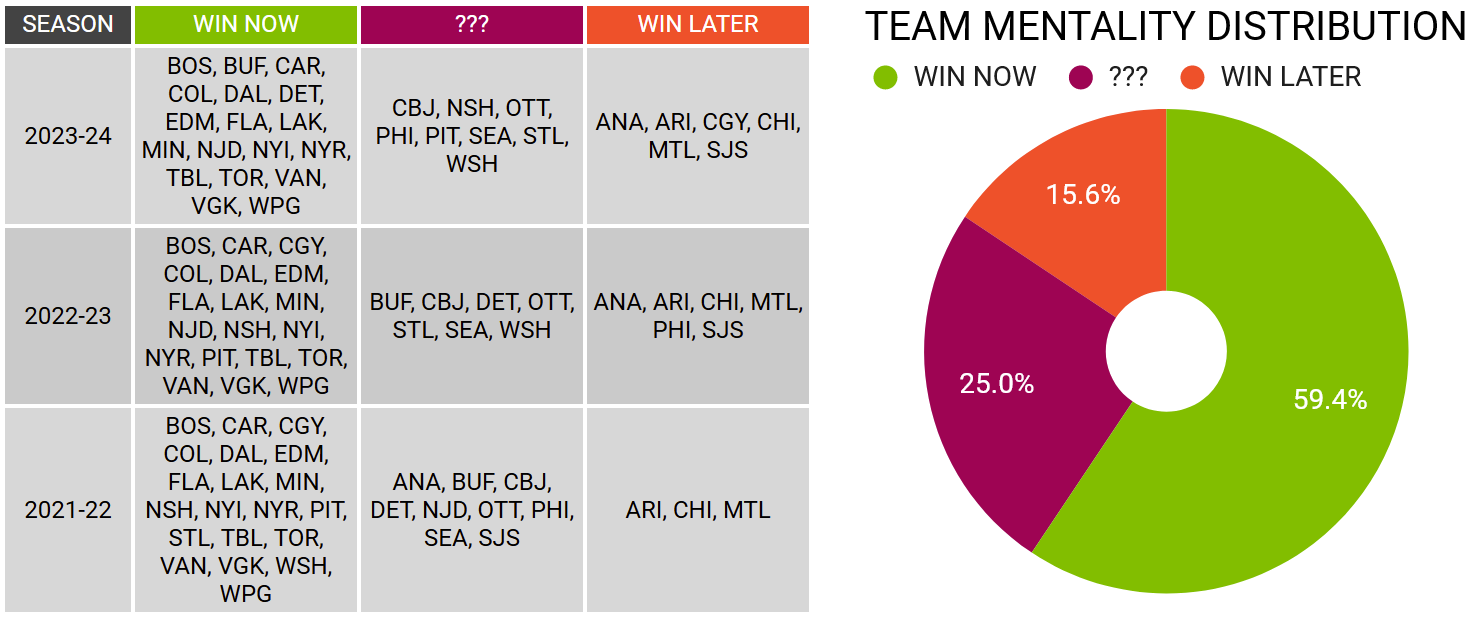

Do these two categories of teams cancel out? To find out, I labeled all teams as either win now or win later based on what I thought each team’s mindset was in each of the last three seasons. I also assigned a ??? label to teams I was uncertain for. It looks like this:

Your mileage probably varies as to who should fall into which category, but the overall trend is clear: far more teams are in win now mode than win later mode. It stands to reason that since there are more win now teams than win later teams, and since winning now involves valuing the future less than the present, the value of future picks is reduced on the market overall.

Final Thoughts

Thanks to everyone who used our tools and/or got through these articles. And once more, thanks to PuckPedia for allowing me to use their data and for making these tools and series of articles possible.